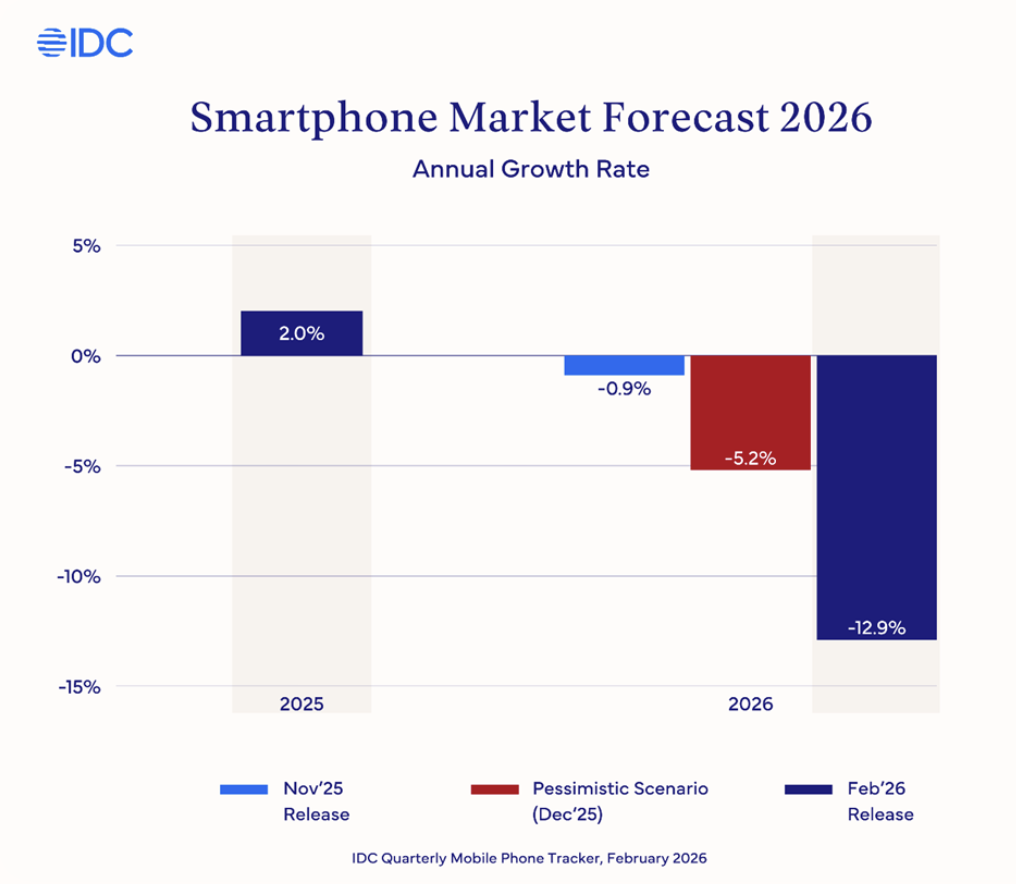

The global smartphone market faces a prolonged memory shortage that will pressure device prices and specifications through at least 2026 and likely into 2027, according to a new forecast from industry analyst firm IDC. The firm warns this will shift market share toward the largest brands and force a structural reset of the industry.

IDC Vice President of Client Devices Francisco Jeronimo described the situation as a “tsunami-like” shock to the consumer electronics industry, with ripple effects for consumers and enterprises expected in the coming months. The core issue is a structural supply crunch where booming demand for DRAM and NAND memory from artificial intelligence infrastructure is directly competing with smartphone and PC manufacturers for limited production capacity.

AI Infrastructure Strains Memory Supply

IDC states that hyperscale data centers building out AI capacity are consuming huge volumes of memory, leaving consumer device makers to fight over the remaining supply. While new fabrication plants and smaller Chinese suppliers may add some capacity, IDC analysts say it will not be sufficient to alter the overall trajectory of the shortage. Memory prices are expected to remain elevated, and IDC does not anticipate a return to 2025 price levels within its current forecast horizon.

Impact on Smartphone Specifications and Pricing

In response to rising component costs, IDC expects some new smartphone models to launch with lower memory configurations rather than manufacturers absorbing the full cost increase. A device that might have shipped last year with 12GB of RAM and 256GB of storage could now be offered with 8GB and 128GB at the same, or even a higher, price point.

The impact is predicted to be most severe in the budget segment of the market, where profit margins are already minimal. IDC estimates over 360 million smartphones priced below $150 shipped globally last year, representing a significant volume in emerging markets. This price band may become economically unsustainable, forcing vendors to either drastically cut specifications or raise prices above $200, where consumer demand is considerably weaker. Some manufacturers may exit these market tiers entirely.

Market Consolidation and Consumer Shifts

Companies with greater financial resources and stronger supplier relationships will be best positioned to secure necessary memory allocations. IDC predicts meaningful market share gains for the largest global original equipment manufacturers in 2026, as smaller and regional players struggle to compete.

This dynamic is expected to lead to several knock-on effects. Consumers may delay purchases, leading to longer device upgrade cycles. There could also be increased interest in refurbished and used smartphones. Furthermore, the total addressable market in emerging economies could shrink. IDC notes that price-sensitive buyers may hold onto devices longer, turn to refurbished models, or, in some cases, revert to basic feature phones if ultra-low-cost smartphones disappear from the market.

Additional Pressure from Trade Policy

Trade policy is compounding the supply challenge. IDC points to new U.S. tariff proposals that could add up to 15 percent to import costs on top of rising component prices. This additional layer of uncertainty makes pricing and sourcing decisions even more difficult for device vendors and their channel partners.

An Industry Facing Structural Change

IDC’s assessment concludes that the smartphone market is heading for a structural reset in terms of its overall size, product mix, and competitive dynamics. With memory shortages projected to last well into 2027, vendors, distributors, and retailers should prepare for a period of sustained turbulence. The firm’s analysis suggests the industry’s landscape will be notably different on the other side of this prolonged shortage.

Source: IDC